The recent movements in the Bitcoin market are largely attributed to significant events involving Mt. Gox and the German government offloading their Bitcoin holdings. A deeper dive into these events reveals a complex interplay of market forces that investors need to be aware of.

Mt. Gox's Bitcoin Distribution Phases

Mt. Gox, which holds 141,000 BTC, is set to return these to creditors in a structured manner. To put this into perspective, all Bitcoin spot ETFs have accumulated a total of 867,000 BTC, with the BlackRock ETF alone holding 304,000 BTC. The distribution from Mt. Gox will occur in three phases, with the first phase happening between July and October, involving 71,403 BTC.

Potential Market Impact

Contrary to fears, it's unlikely that all 70,000 BTC will hit the market simultaneously. Many creditors, especially long-term holders, may choose to hold onto their Bitcoin rather than sell immediately. Those BTC acquired by claims agents might be sold more quickly but in a responsible manner. Considering the current market, if even 50% of these BTC are sold, that's 35,700 BTC, valued at approximately USD 2.1 billion.

Market Absorption Capacity

The market has shown it can handle a daily sell pressure of 6,000-10,000 BTC, and during high ETF inflows, up to 15,000-25,000 BTC. Therefore, the sale of 35,700 BTC from Mt. Gox might not be as disruptive as anticipated. The current market downturn may be more influenced by fear and overestimation rather than actual sell pressure.

Germany’s Bitcoin Holdings Strategy

Germany holds about one-fourth of the Bitcoin that Mt. Gox does. Despite the German government’s apparent aversion to Bitcoin, their preference for cash means they are likely to sell their holdings strategically at higher prices. This suggests a phased selling approach rather than a market dump, mitigating potential adverse effects on Bitcoin prices.

Long-Term Market Outlook

In the broader context, this cycle of unique selling pressure is reminiscent of past anomalies, such as the COVID crash. Looking forward, positive market drivers include the growing influence of Bitcoin ETFs, upcoming elections that may herald political shifts favorable to crypto, and the potential recycling of USD 16 billion in FTX repayments back into the crypto market.

Understanding these dynamics is crucial for investors navigating the current Bitcoin landscape. By analyzing the structured distribution from Mt. Gox and Germany's strategic selling, investors can better gauge the potential impacts and prepare for market fluctuations.

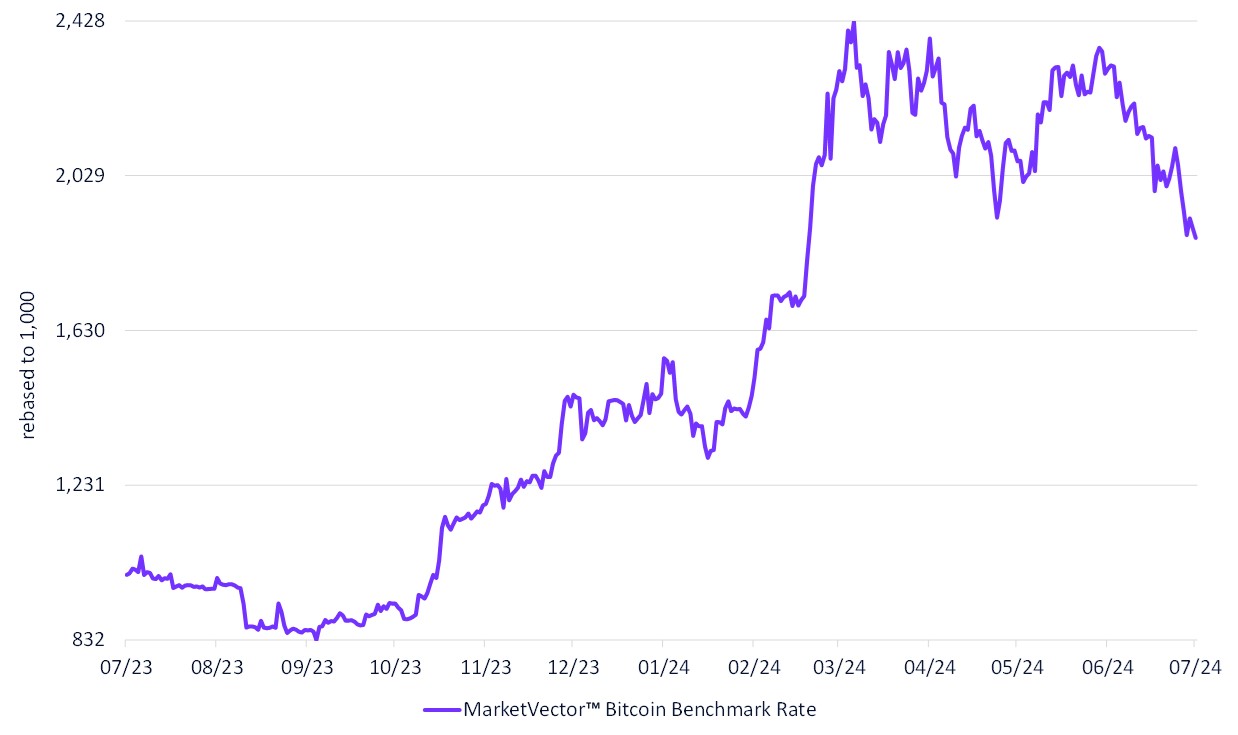

MarketVectorTM Bitcoin Benchmark Rate

Source: MarketVector. Data as of July 8, 2024.

For more information on our family of indexes, visit www.marketvector.com.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine