The tables below shows fundamental data of the Index.

Descriptive values are updated on a daily basis. The chart shows historical values on a monthly basis.

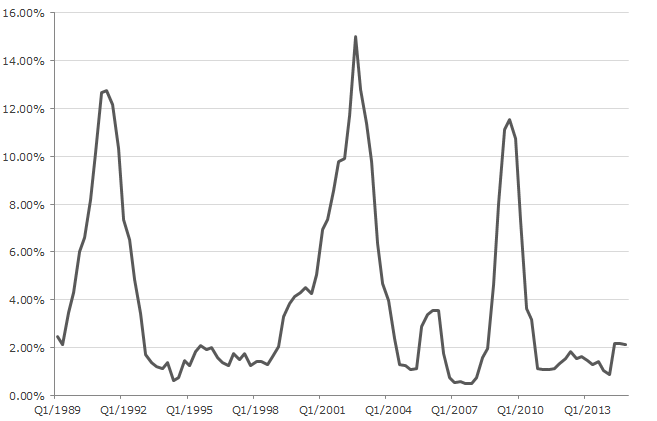

Altman-Kuehne/NYU-Salomon Center Dollar-Based 12-month Moving Average Default Rate Index

Altman-Kuehne/NYU-Salomon Center Dollar-Based 12-month Moving Average Default Rate is calculated by adding the defaults in a given quarter (3 months) to the total dollar amount of defaults from the three prior quarters (nine months), and then dividing the total by the size of the high-yield market at the beginning of the quarter for which the rate is being calculated. This rate, as well as historical default rates, is published every quarter in our "Defaults and Returns in the High-Yield Bond Market" reports, available by subscription from the Salomon Center.

Source: Altman, Edward I. and Brenda J. Kuehne. Data as of 31 December 2014

The tables below shows Bloomberg Composite Rating breakdown of the index components.

The data are updated on a daily basis.