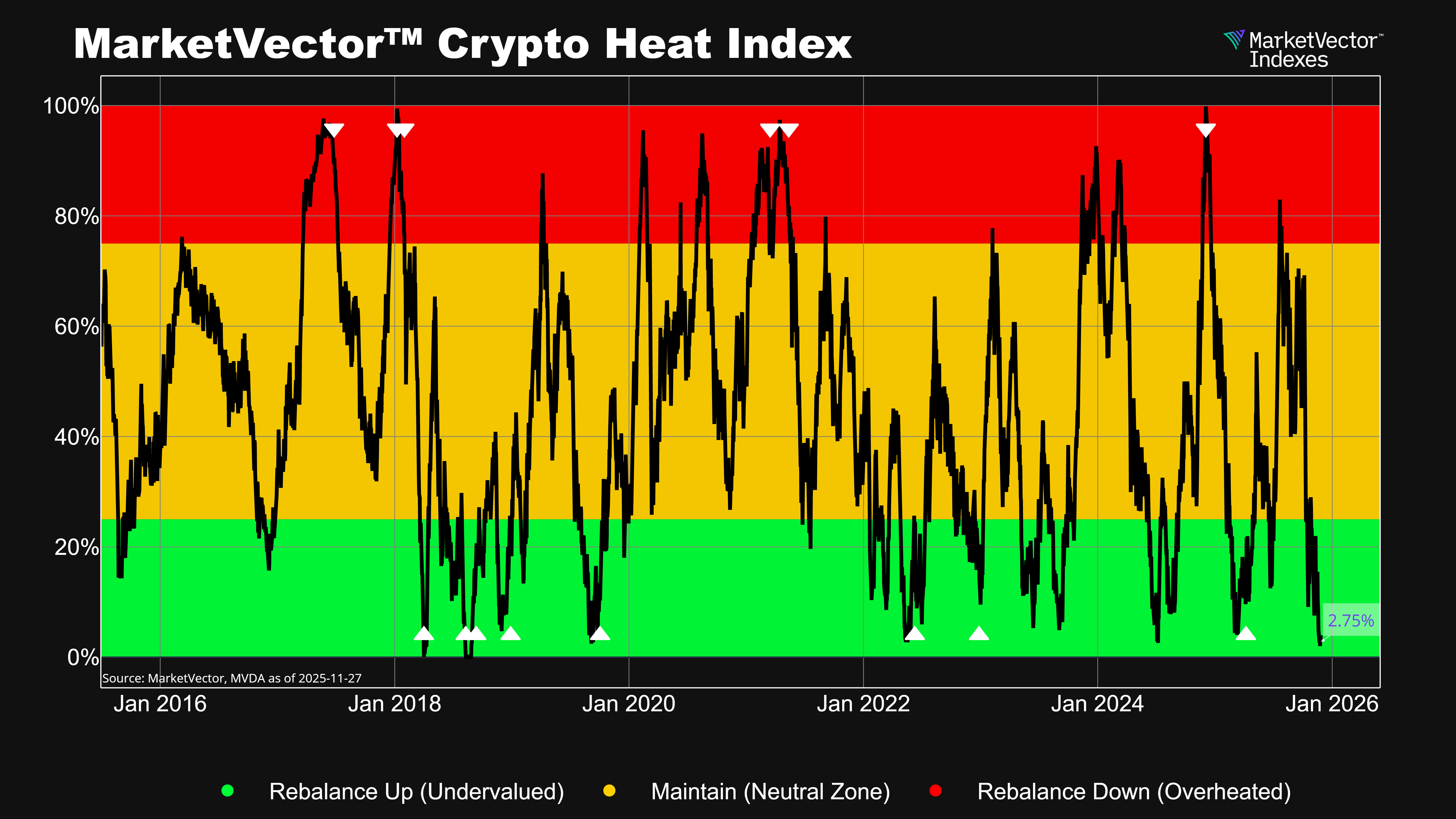

A protocol can earn a portion of its revenue, known as Real Yield, by deploying or locking its governance token. In contrast to revenue obtained through the issuance of tokens, the Real Yield is a return that results from producing real revenue. This system is called DeFi 2.0 and distributes revenue in the form of a dominant token, either ETH or USDC.

Additionally, Real Yield paves the path for users to pay with the tokens of their choice by allowing them to participate in the platform's earnings. The return provided to users increases in direct proportion to a cryptocurrency project's revenue generation. In order to reward token holders, individuals who wager on real yield projects wager on their capacity to draw in new users and grow their revenue over time.

Why Real Yield?

Because it varies from traditional user acquisition we know from the early DeFi protocols, Real Yield is a game-changer. In the early days, to boost the amount of user cash deposited, investors received excessively inflated, unsustainable annual returns. Even if the returns are alluring to investors, they cannot be maintained by issuance of tokens or fraudulent returns.

Higher inflation issuances are not required for a project that exhibits the traits of a true return. These genuine initiatives produce returns through real income are gaining momentum. They have more advantages and offer leveraged trading with abundant liquidity and affordable costs. These include the DEXs such as DYDX, GMX, GNS, SNX, and UMAMI. The success of the derivatives exchange GMX and its cash flow token model has recently made it a shining example of Real Yield. Liquidity providers get 70% of GMX's revenue in the form of the token GLP. The other 30% is given to users who lock up their GMX tokens in the form of ETH or AVAX, depending on the chain.

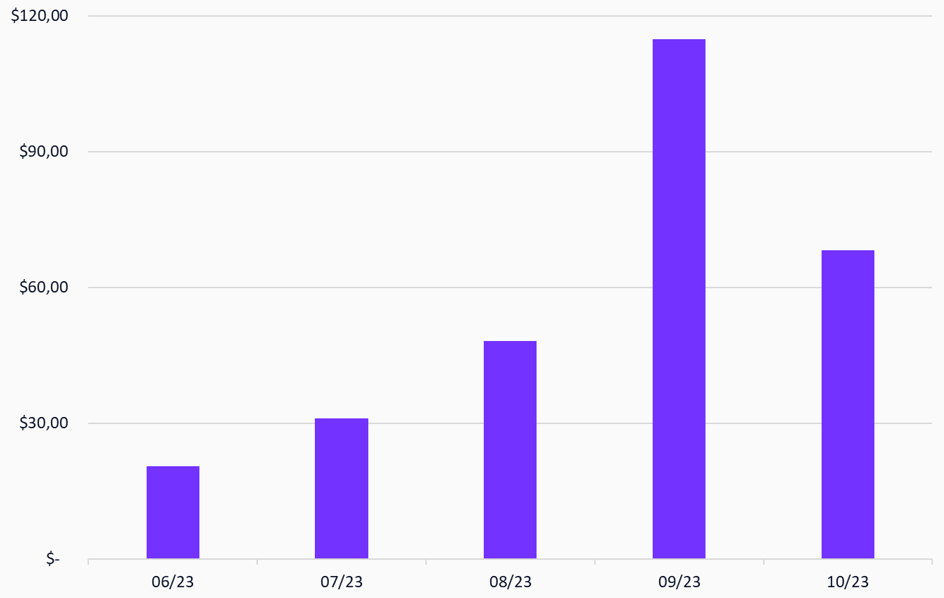

A quick calculation can reveal whether the project is viable and capable of producing actual results. Knowing how much of their revenue is retained in relation to how much of a token is emitted is another crucial ratio. Numerous large DEXs brag about their high TVL and revenue, but these figures pale in comparison to the value of tokens used as subsidies. With $114 in revenue per GMX token in September and $68 in October, GMX has a reputation for its ability to provide token holders with a high return (Exhibit 1).

Exhibit 1: esGMX Arbitrum - Protocol Revenue Per esGMX Token Emitted (Monthly)

Source: Blockworks, Dune Analytics. Data as of November 04, 2023.

Regardless of how juicy the yield appears, it is essential for investors to evaluate the business model and ensure its viability. People should utilize the token because they use the protocol, not because they are just speculating on its price and yield.

Exhibit 2: MVIS® CryptoCompare Decentralized Finance Index

Source: MarketVector IndexesTM, data as of November 7, 2022.

Get the latest news & insights from MarketVector

Get the newsletterRelated: