By driving down the costs of financing,ultra-low interest rates have been supposed to deter savings and encourageborrowing, therefore stimulating the economy through increased consumption andinvestment.

It would appear, though, that in anumber of countries with negative interest rate policies (NIRPs), for example,Denmark, Sweden, and Switzerland, exactly the opposite has happened.1)

As far back as April 2015, the Bank forInternational Settlements noted that, in such environments, “Ultra-low or negative interest rates willadd to their [households’] worries bymaking it more difficult for them to build up enough retirement savings. Thus householdsare more likely to increase their savings rate then reduce it.” 2)

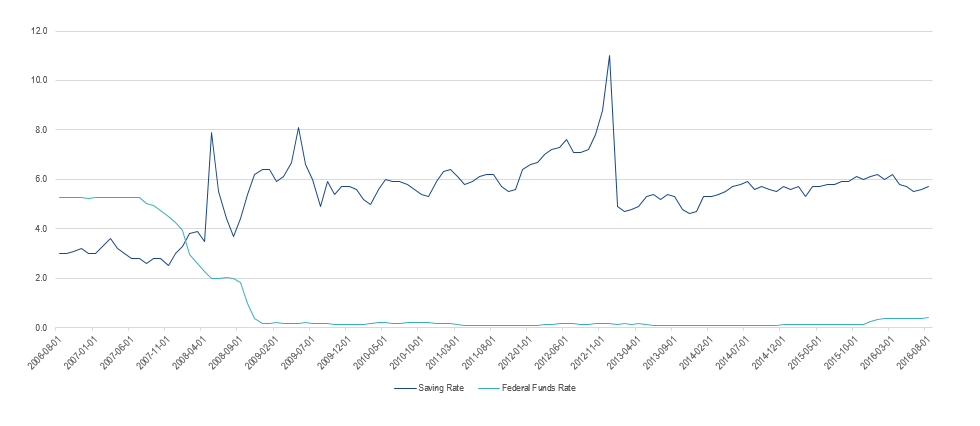

Even in the U.S. over the past severalyears there has been no evident trend of a decreasing saving rate. The questionis, now: What can central banks do instead?

U.S. Personal Saving Rate3)

vs.

Effective Federal Fund Rate4)

Source: Federal Reserve Bank of St. Louis

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine