After a short-lived, CPI-fueled dump, crypto rallied impressively from the lows. The headline about a loose confirmation on the Merge's target date accelerated the positive momentum. In our last blog post, we’ve written about the misconceptions of this sophisticated project. It is undoubtedly one of the biggest events in crypto’s history and has the potential to bring outperformance to ETH.

According to Tim Beiko, who is an Ethereum protocol support engineer, the Merge may take place on the week of September 19. It’ll see Ethereum move from the energy-intensive Proof-of-Work consensus mechanism to a more efficient Proof-of-Stake system. While it’s not expected to reduce Ethereum's fees and slow transaction speeds, it will have a significant impact on the network's energy use.

The market is so excited because it’s expected that there will be a large supply sink post-merge due to the depreciation of PoW block subsidies and indefinitely locked validator rewards in conjunction with base fee burns. Not only will the total ETH supply become net deflationary, but liquid rewards earned by validators will be reduced from 15,135 ETH per day to 1,777 ETH per day. Validators also have far lower operating costs and a literal stake in the network, so it’s reasonable to assume these players are generally bullish on ETH.

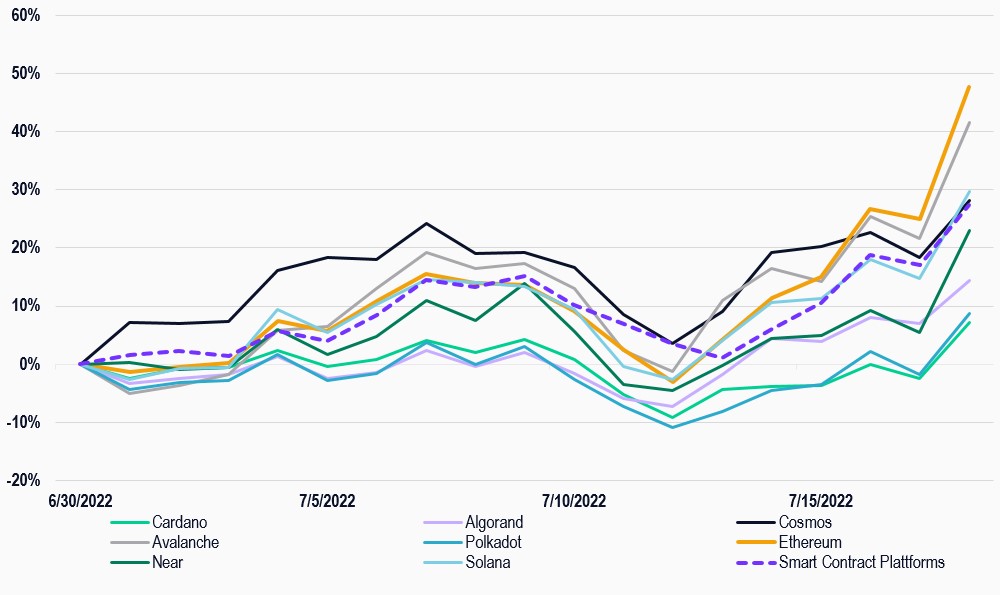

The following chart indicates how theses news impacted the whole smart contract category with Ethereum outperforming the rest of the coins. Notable other outliers to the upside are Cosmos and Avalanche. Polkadot and Cardano are the laggards. It’s a good sign that fundamental data have an impact again. The Merge has filled a narrative void, however Crypto has become a macro asset. It remains to be seen, if such news can impact the market sustainably. At least with the help of our MVIS® CryptoCompare Smart Contract Leaders index (ticker: MVSCLE), investors can easily discover, which coins are outperforming the market or not. A great help in a very volatile cycle we’re currently in.

Cumulative Performance of Smart Contract Coins and the MVIS® CryptoCompare Smart Contract Leaders

Source: MarketVector Indexes. All values are rebased to 100. Data as of July 18, 2022.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine