U.S. steel producers are facing a tough time. Weekly production has fallen to levels not seen in a number of years and, at the same time, imports have soared.

For the first two months of 2015, finished and total steel imports were up 36% and 24% respectively from the same period last year. And the estimate was that, in February, the market share of finished steel imports was some 33%.

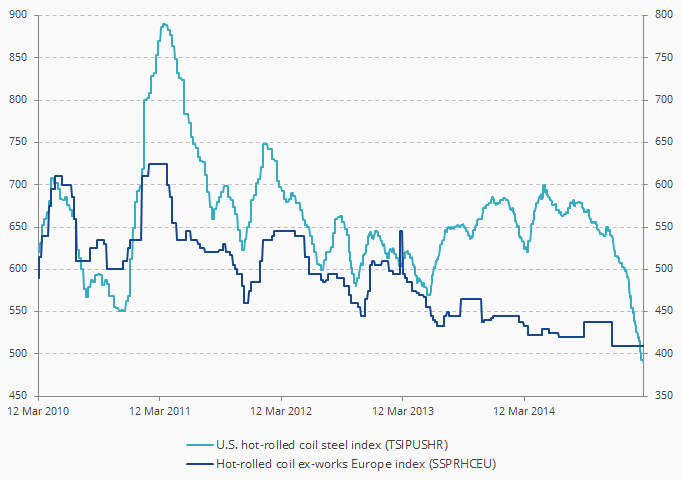

The silver lining, however, is that production is down. By the end of February, total weekly steel production in the U.S. had fallen by 3.4% bringing it to its lowest level for five years, but indicating that the industry is responding.Furthermore, the surge in imports was driven by U.S./global pricing differentials which now no longer exist and demand in the U.S. (except from the energy sector) is reasonably strong.

Steel Pricing Differentials

Source: Bloomberg, data as of 6 March 2015

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine