Second quarter reporting concluded in August and the reports were not pretty. Companies were hit by the combination of falling metals prices and rising costs. This lead to earnings misses and cost revisions. Most companies moved cost expectations to the upper end of guidance or revised them higher. We don’t fault the companies because most of the cost pressures are out of their control.

A war in Ukraine wasn’t factored into anybody’s guidance in January. Fuel, energy, and consumables that are tied to the petrochemical chain are some of the main cost drivers. Another is tight labor, which is a global phenomenon. Original company guidance called for 3% to 6% 2022 cost inflation, but those estimates have doubled and all-in sustaining costs now average around $1,200 per ounce.

While margins remain healthy enough to support dividend policies and many companies continue to buy back stock, the uncertainty of how long this rising cost environment will last appears to be largely priced into gold stocks.

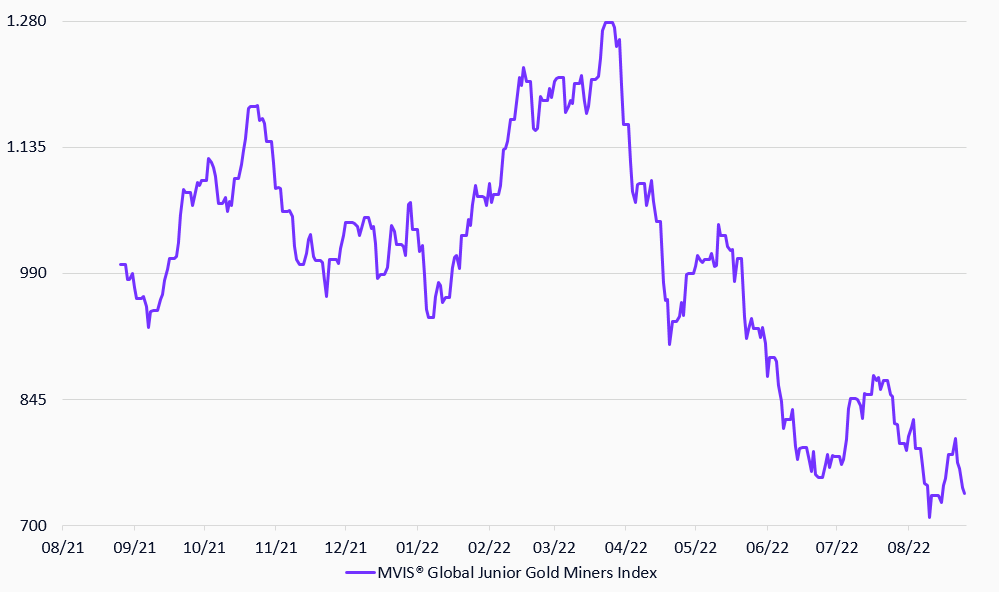

MVIS® Global Junior Gold Miners Index

9/19/2021-9/19/2022

Source: MarketVector Indexes. All values are rebased to 1,000. Data as of September 19, 2022.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine