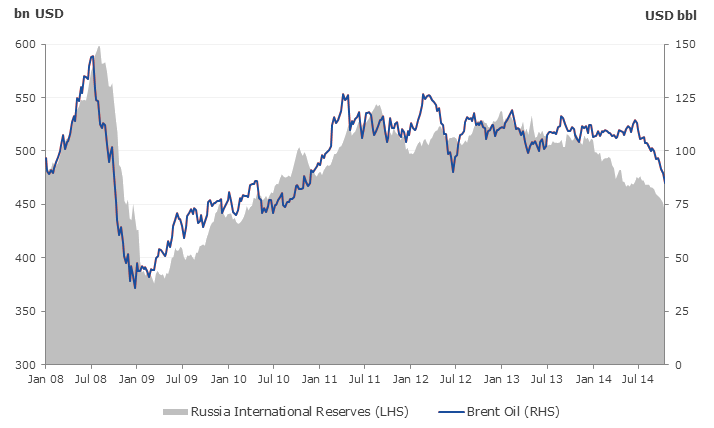

Russia's political and economic outlooks remain precarious. There is no obvious way to resolve the Ukrainian crisis which means that sanctions will not be lifted any time soon. This will continue to weigh on Russia's growth while keeping inflation pressures up. One piece of good news is that Russia's current account is in surplus for now. However, capital outflows are large and the CBR is losing reserves at an alarming rate trying to prop up RUB. Lower oil prices also pose risk to Russia's external balance. Even though Russia's international reserves are still around 20% of GDP – multiple claims on them are likely to increase if Russian companies and banks remain cut off from global financial markets.

Russia: Reserves and Oil

Source: Bloomberg

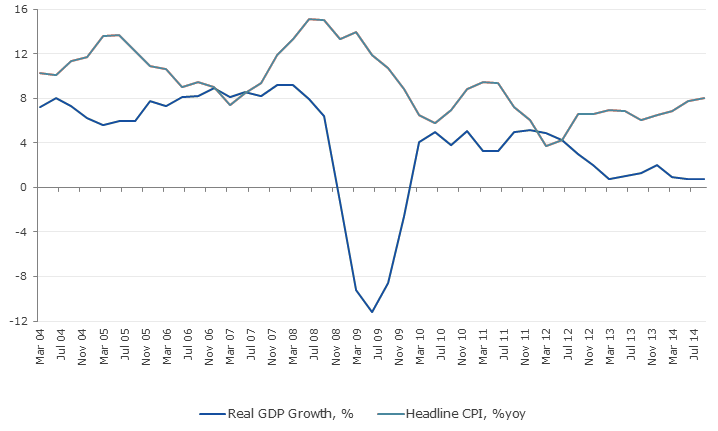

Russia: Real GDP Growth and Inflation

Source: Bloomberg

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine