The ruble is under pressure and recent actions by the U.S. State Department have not helped. It recently sent Congress a list of entities linked to the defense and intelligence arms of the Russian government that “will guide sanctions the administration must begin to take on Jan. 29, 2018.” 1

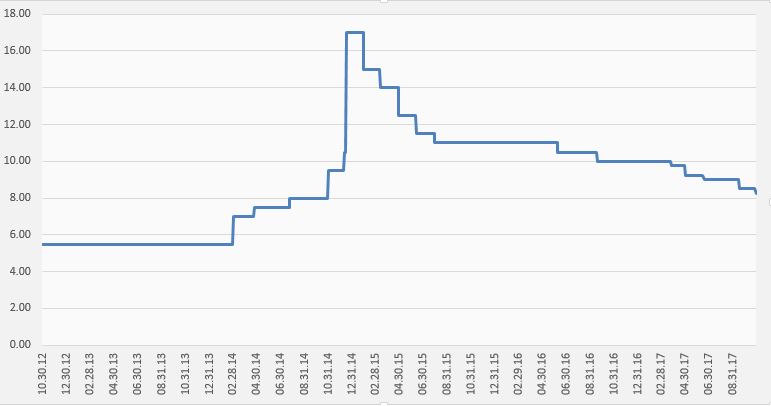

The question is whether such reaction is justified policy-wise. On October 27, Russia’s central bank cut its policy rate by a cautious 25bps (down to 8.25%), thereby reaffirming its orthodox credentials. The bank’s move reflects its concerns about both the nature and the sustainability of disinflation (i.e. mostly food prices or something more permanent). In addition, the bank’s measure of inflation expectations stopped falling in September – edging up to 9.6%.

It will be interesting to see when, or if, this pressure lifts.

Central Bank of Russia - One Week Auction Rate (%)

Source: FactSet

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine