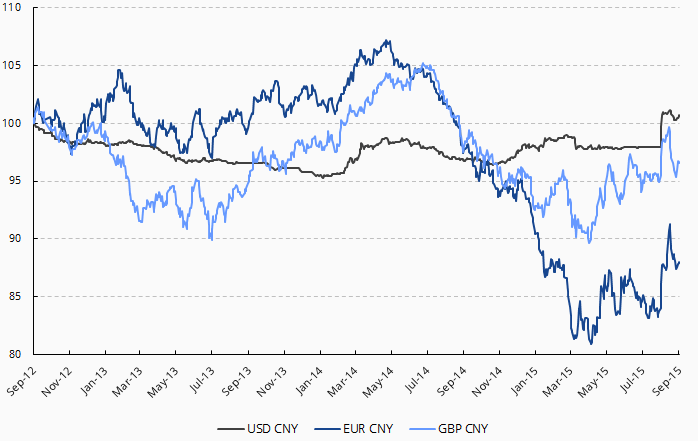

On 11 August, the People’s Bank of China (PBoC) lowered its renminbi central reference rate to the weakest level since 25 April 2013, and announced a partial liberalization of its exchange rate controls. We see the weaker Renminbi reference rate as simultaneously boosting China’s export growth and, by improving exchange rate flexibility, raising the likelihood that the International Monetary Fund (IMF) will be willing to include the Renminbi into its special drawing rights (SDR) basket.

Source: Bloomberg, Data as of 10 Sep 2015

We believe the devaluation may continue slowly by the end of this year, with the short-term goal of improving market sentiment in response to concerns over economic slowdown, and the upcoming US interest rate hike. We do not see long-term depreciatory pressure from the market; to the contrary, given China's economic prospects, we see the liberalization of the renminbi exchange rate as likely to result in a long-term appreciation of the Chinese currency.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine