A banking crisis is inherently deflationary, a fact even ChatGPT would confirm. As the banking crisis unfolds, the Federal Reserve has reported that US banks borrowed $475 billion just last week. In the wake of SVB's collapse, over $500 billion has been withdrawn from small banks in merely two weeks.

The Hunt for Yield: Where are Withdrawals Heading?

Withdrawing individuals and institutions are now seeking yield, turning to alternatives like T-Bills, Money Market Funds, and Ultra-Short-Term ETFs. This shift in behavior is unlikely to reverse course until deposit rates can compete with market rates, making deposit outflows a persistent issue for banks.

The Fed's Role and Bitcoin's Unique Position

As central banks, particularly the Fed, contemplate new easing measures, Bitcoin's position among risk assets becomes increasingly noteworthy. While Bitcoin is a risk asset due to its volatility, it lacks the vulnerabilities of stocks and bonds, such as earnings or credit ratings. In reality, Bitcoin is largely disconnected from the real economy, with liquidity flows being the primary influence on its performance.

Bitcoin's Allure in a Fragile Corporate Landscape

During periods of downgraded earnings expectations and corporate fragility, a "pure play" asset like Bitcoin becomes even more appealing to macro investors. Signs of this trend are already visible, with Bitcoin outperforming other crypto assets and an uptick in spot and derivatives trading volumes. As the Fed may soon need to bolster banks' collateral once more, the influx of liquidity stands to benefit all assets, with Bitcoin being a prime beneficiary.

In conclusion, understanding the current banking crisis and its deflationary nature is crucial to navigating the evolving crypto investment landscape. As traditional financial institutions grapple with deposit outflows and central banks mull easing measures, Bitcoin's unique position and detachment from the real economy make it an increasingly attractive option for macro investors.

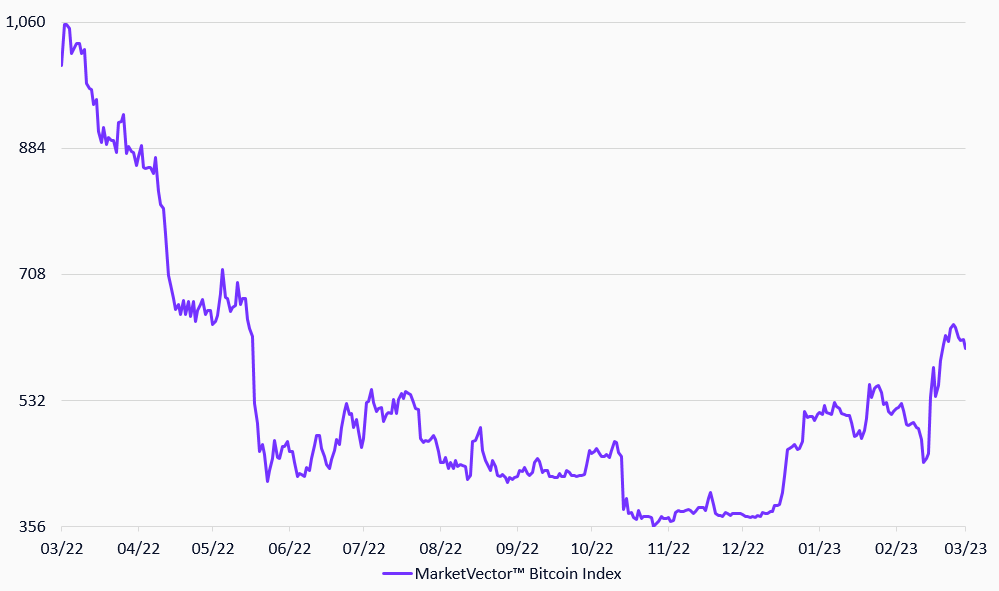

MarketVectorTM Bitcoin Index

27/3/2022-27/3/2023

Source: MarketVector IndexesTM. Data as of March 27, 2023.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine