Since ancient times when the Babylonians and early Chinese insured shipping losses, insurance has worked as a business model because insurers’ gains from premiums generally exceed claims from losses. Insurers manage risk and profitability by constantly re-pricing premiums and diversifying their portfolios. The Market Vectors US Volatility Premium Capture Index (MVVCAP) is a simple implementation of a hedge fund strategy that sells put options on a diversified portfolio of stocks as a form of portfolio insurance to investors with a visceral need to calm their fears of market volatility. Put option premiums constantly re-price to reflect latest market volatility, and tend to climb following market corrections.

Source: Bloomberg, SPTR Index, MVVCAP Index

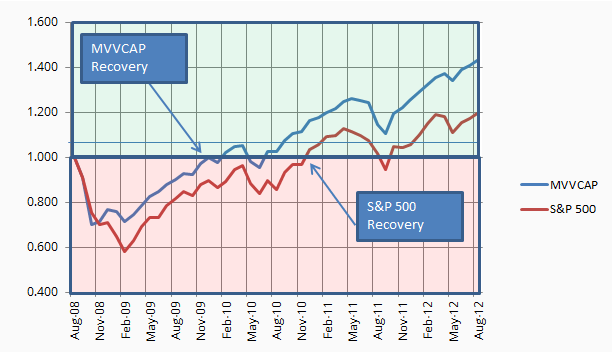

Stress Test: Following the 2008 Financial Crisis, hefty premiums helped MVVCAP recover in 13 months vs. more than 2 years for S&P 500.

For the past 9-year period 31 Dec 2005 - 31 Dec 2014, MVVCAP had higher annualized return and lower standard deviation than S&P 500.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine