We view gold equities at present as generally undervalued, trading at low multiples both historically for the industry and relative to gold. We believe this valuation gap provides an opportunity for gold equities to outperform gold even in a sideways gold price environment, especially if that price action develops around the USD 2,000 an-ounce level.

Industry cost inflation has mostly subsided, and operating costs appear to be contained, with all-in-sustaining costs on average at around USD 1,300 per ounce. While we reiterate our outlook for higher gold prices in 2024, we want to highlight that at current spot gold prices of around USD 2,040 per ounce, the gold miners, as a group, should be able to enjoy margin expansion and enhanced free cash flow generation this year.

We expect gold companies to have the ability to produce solid operating and financial results that can withstand the volatility of the gold price and demonstrate that they can sustainably operate profitable businesses throughout the cycles. We believe that consistently proving this resilience to the markets should lead to increased incorporation of gold equities as an asset class in the broader investment universe and lead to a rerating of the gold mining sector.

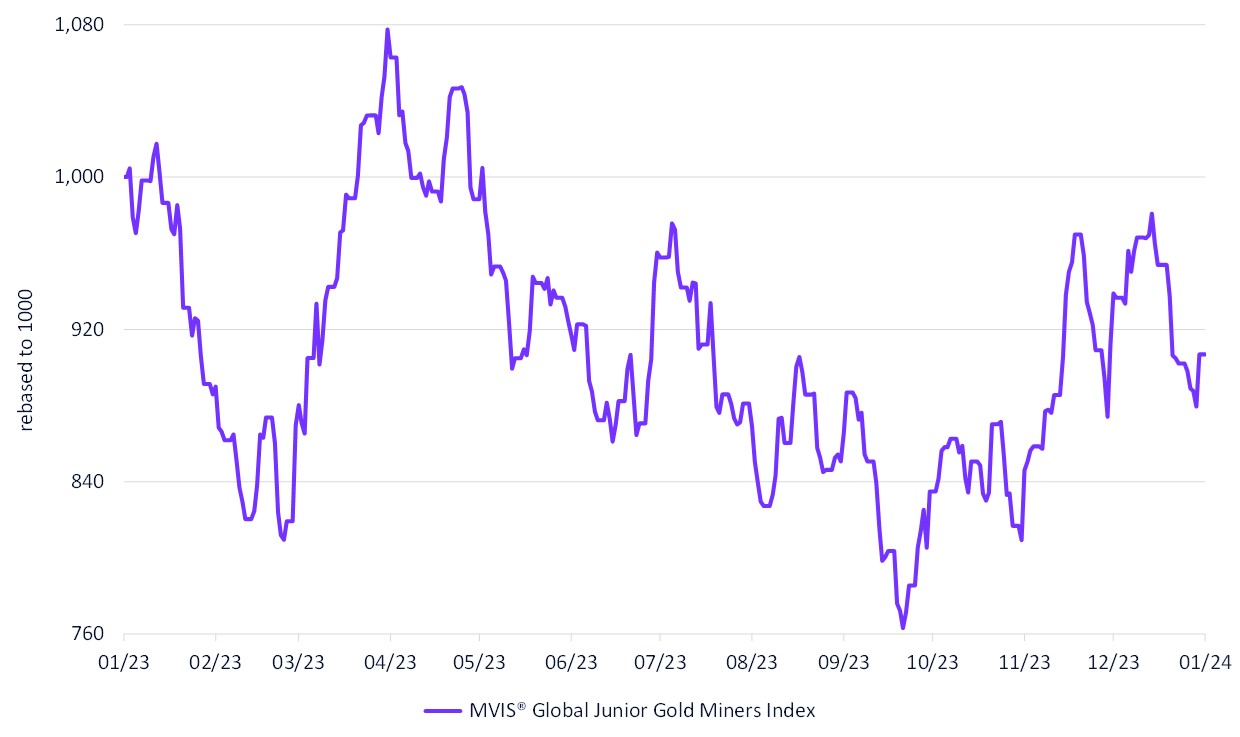

MVIS® Global Junior Gold Miners Index

1/14/2023-1/14/2024

Source: MarketVector IndexesTM. All values are rebased to 1,000. Data as of January 14, 2024.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine