The World Gold Council reported a total gold demand in 2023 of 4,899 tonnes. This was the highest on record and 3% above demand in 2022. Excluding what it refers to as OTC (over-the-counter) or off-exchange transactions (an estimate that captures the difference between gold supply and demand), 2023 demand was a bit (-5%) below 2022, but still very strong.

We have been highlighting the following changing gold demand dynamics as being at play: Strong central bank buying as a dominant driver of gold prices in 2023, with demand from the official sector representing over 20% of total gold demand for the year. While net purchases of 1,037 tonnes in 2023 fell just short of the record 1,082 tonnes central banks purchased in 2022, the figure is more than double the pre-2022 annual average net purchases of about 500 tonnes of gold per year.

This is an impressive trend. And is expected to continue in the longer term. In contrast, holdings of global gold bullion ETFs continued to see outflows in 2023, dropping by 244 tonnes, driving total investment demand to a 10-year low, another reflection of investor’s apathy towards gold as an asset class.

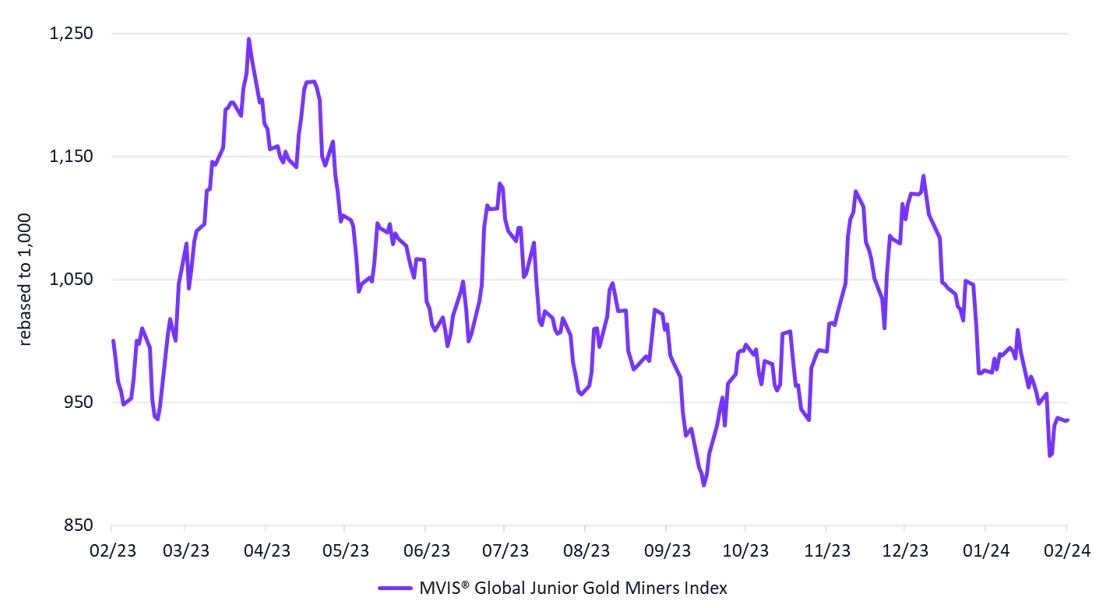

MVIS® Global Junior Gold Miners Index

02/20/2023 - 02/20/2024

Source: MarketVector. All values are rebased to 1,000. Data as of February 21, 2024.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine