Brazil is a net sovereign creditor in U.S. dollars: It has larger U.S. dollar reserves (USD 350bn) than external debt (at USD 150bn) which can be positive for external debt in two ways. First, it describes literal solvency – the country is able to pay its external obligations. Second, a country with an active debt management policy will purchase bonds, raising their price (all things being equal, of course) and reducing the country’s debt.

Net creditor status, though, does not mean that a country has no problems. Brazil, for example, is increasing its local currency debt significantly. However, if a country’s central bank has a floating exchange rate, it will tend to leave reserves alone, and not defend a particular exchange rate. This increase in local debt, then, becomes largely irrelevant for external obligations, because reserves stay the same, as does external debt.

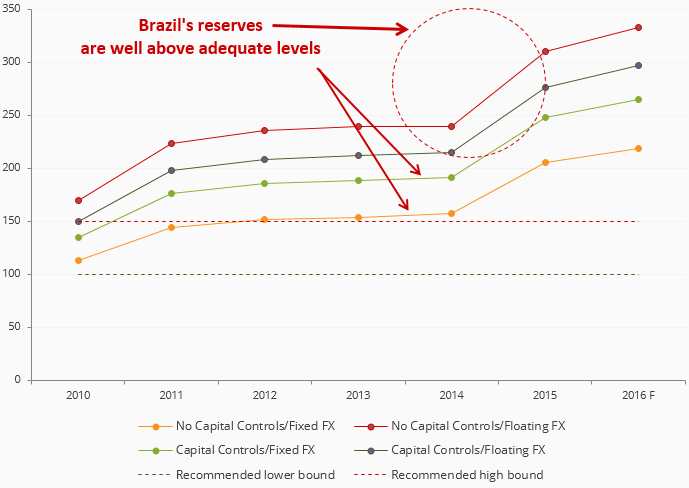

Brazil – International Reserves as % of Recommended (Adequate) Reserves

Source: Van Eck Research, Bloomberg, IMF, WB

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine