The narrative for Ethereum remains strong. It’s the go-to smart contract platform. Users are clearly willing to pay fees on the network for trading, NFT’s and transferring assets. This high demand comes with high fees though. While smaller users are priced out, institutions are willing to pay the high gas price in order to have faster settlement or doing large transactions on a more secure network. While Layer2 scaling is an important topic for the development for Ethereum, the current demand for this layer-1 platform has a direct effect on the supply as well.

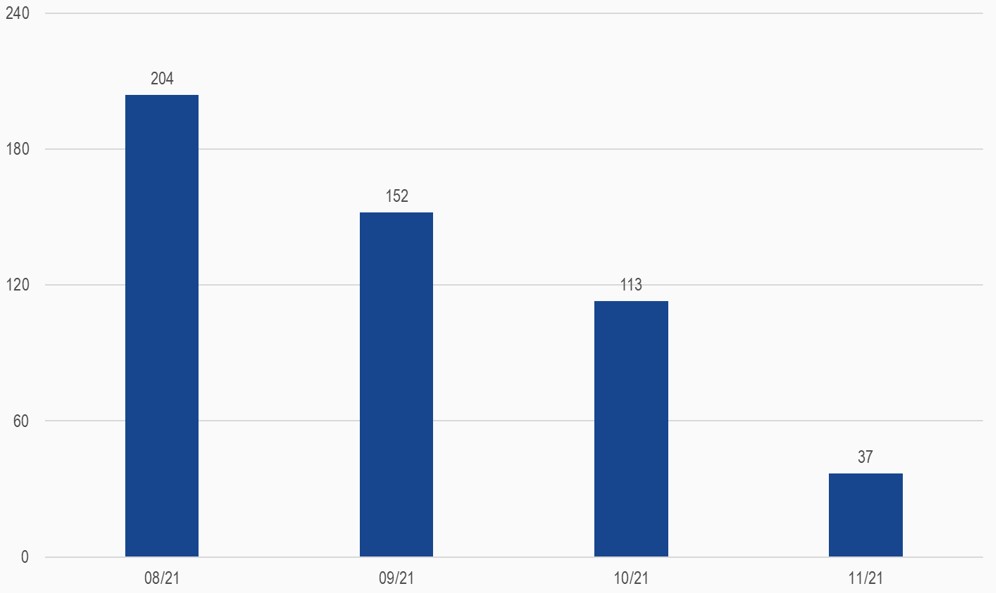

The latest change of Ethereum’s transaction fee system – EIP-1559 leads to a fee burn of the base fee. At the moment, the fee burns are so high, that the net issuance of ETH continues to decline.

Ether Net Issuance (in thousands of ETH)

31/8/2021-30/11/2021

Source: Watch The Burn, messari.io. Data as of 3 December 2021.

So reduced supply and increased demand are the perfect prerequisite for an ongoing rally. While the crypto market is in a correction phase, Ethereum is doing incredibly well (10.43% down from All-Time-High), especially when you compare that to the old market leader Bitcoin (26.46% down from All-Time-High). If this transaction demand continuous, Ethereum could experience negative net issuance in December. These ongoing demand supply dynamics should support the Ethereum price even further.

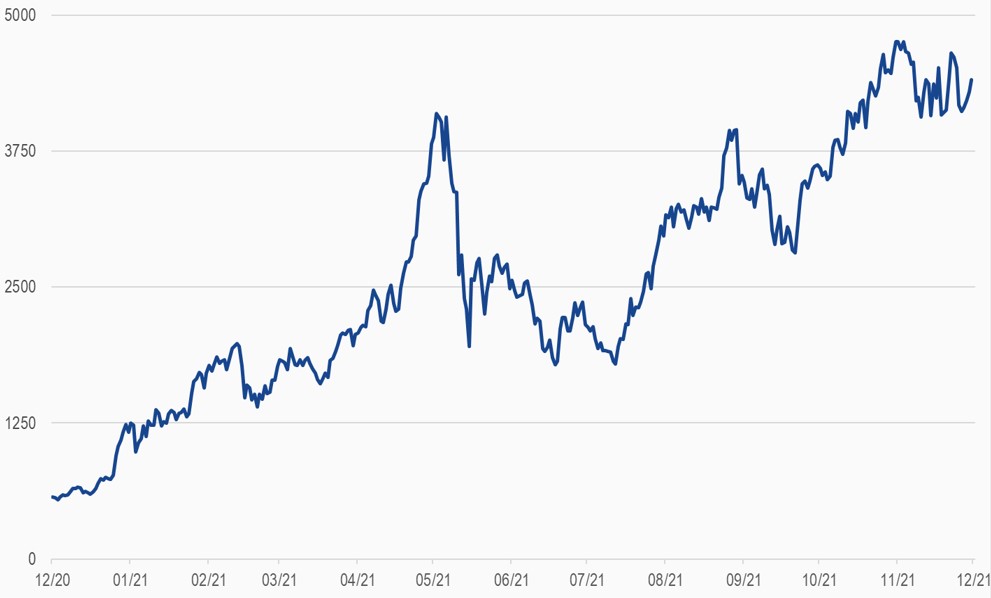

MVIS CryptoCompare Ethereum Benchmark Rate Index

09/12/2020-09/12/2021

Source: MV Index Solutions. Data as of 9 December 2021.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryGoal! Small Country, Big Impact

-

Commentary

CommentaryHidden GEMs: Ukraine